In 2015, the East African Community Council of Ministers adopted the East African Community Competition (Amendment) bill which provided for the establishment of the East African Community (EAC) Competition Authority (EACCA).1 The competition authority has jurisdiction over all five member states of the EAC; Burundi, Kenya, Rwanda, Tanzania and Uganda. National competition laws and regulations are limited to political boundaries without extended powers to regulate company activities across borders, while the EAC Competition Authority will have jurisdiction over all mergers and enforcement matters with cross-border competition effects.2

This article discusses economic linkages between EAC member states, the history of mergers and acquisitions, as well as competition concerns that motivate the establishment of the authority.

Economic links between the member states

The EACCA had been scheduled to launch in June 2015, however, efforts to operationalise the Act were disrupted by conflicts with competition laws and institutions in the member states.3 It is not clear at this stage when the authority will launch operations in full. The difficulties may have resulted from the fact that some of the countries do not have a background in competition law enforcement, which comes through extended experience in dealing with cases, advocacy and engagement with public and private stakeholders.4 Country institutions may also be under-resourced and not sufficiently capacitated to make decisions independently.5 For example, Rwanda, Uganda and Burundi (each without fully established laws and institutions) failed to submit nominees for the posts of commissioners to the regional competition authority partly because there were no commissioners in their own jurisdictions.6 In addition, differences between countries regarding policies on policy priorities, investments, public procurement, and trade and industry policies within member states creates challenges in adopting a regional competition act which is aligned with national competition laws.7

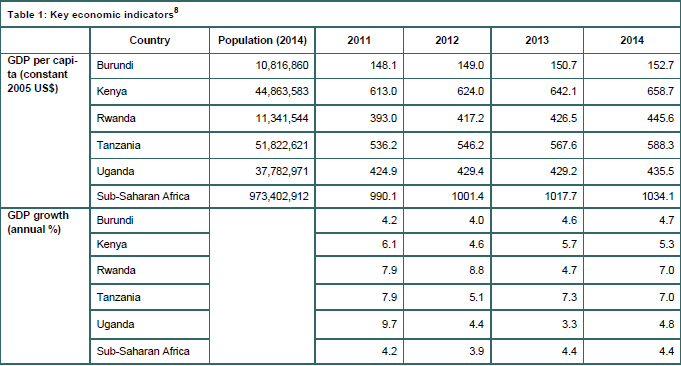

Despite these challenges, common economic linkages between member states make it ideal to operate a regional competition authority in East Africa. The member countries are relatively small economies that share common ports and transport infrastructure. Member states have low levels of economic growth in comparison to other countries in sub-Saharan Africa where the average gross domestic product (GDP) per capita of US$1 034 in 2014 (Table 1). Together, countries in the EAC have an average GDP per capita of US$ 456.16 and an annual GDP growth rate of 5.76 percent per year in 2014. Although the EAC member states have low GDP per capita by country and collectively, economic growth has been significant in the period and faster than the Sub-Saharan Africa average in most cases.

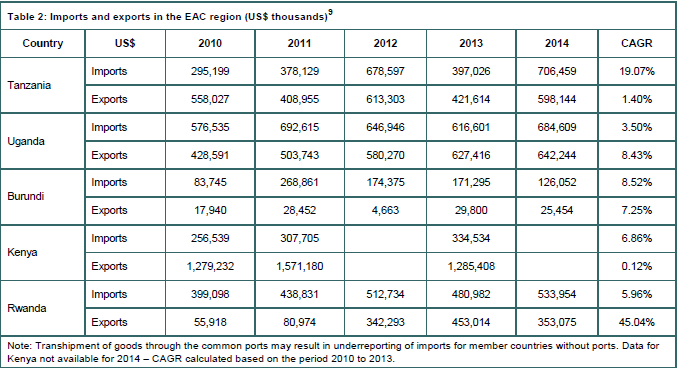

Strong growth coupled with a large combined population of approximately 151 million means that there may be opportu-nities in future for firms to expand and gain economies of scale by accessing the larger regional market. Trade between the countries is also growing, and a customs union has operated in the region since 2005. From 2010 to 2014, imports and exports by member states from others within the region have grown significantly across countries based on the estimated compound annual growth rates (Table 2). Most interesting is the emergence of Rwanda as an exporters into the region (although not at the levels at-tained by Kenya and Tanzania as yet), and the growth of Uganda’s exports as well.

The use of common ports and transport routes, and the cus-toms union, facilitates increased trade between member states and increases the ability of firms to compete across the region.10 Two main transit corridors facilitate imports and exports in the region and there are plans to extend the rail-way line coverage linking all member states.11 The Northern Corridor which starts from the port of Mombasa services Ken-ya, Uganda, Rwanda, Burundi and Eastern Democratic Re-public Of Congo (DRC). The Central Corridor which starts from the port of Dar es Salaam services Tanzania, Zambia, Rwanda, Burundi and Eastern DRC.12

Mergers and acquisitions in the EAC region

In customs unions, there is potentially increased competition between firms as they expand operations across national borders, increase output and exploit opportunities for cost saving in production in a larger market.13 As firms expand across borders they are likely to engage in mergers and ac-quisitions. For example, in the retail industry Kenyan super-market chains such as Tuskys and Nakumatt have opened up several branches across countries in East Africa. Na-kumatt has 52 stores, 34 of which are in Kenya, 9 in Uganda, 3 in Rwanda, 5 in Tanzania, and 1 store in Burundi.14 Tuskys has 44 stores in Kenya and 6 in Uganda.15 Tuskys acquired two Ugandan supermarket chains, Good Price and Half Price, in 2011.16 Both firms have plans for further expansion into the rest of the region.17

In the banking and finance sector, Kenyan banks Kenya Commercial Bank, Equity Bank, Fina Bank and Commercial Bank of Africa have operations in more than three member states with 16 branches in Tanzania, 31 branches in Uganda and 16 branches in Rwanda.18 The telecoms sector has also experienced a number of mergers and acquisitions. In 2012 Airtel with operations in Kenya acquired Warid Telecom in Uganda cementing its position as the second largest player in Uganda’s market.19 Orange Group exited all its East African operations in 2015 when it sold its 70% stake in Telkom Ken-ya to Helios and its operations in Uganda to Africell.20 In mo-bile money services, cross-border transactions are increas-ingly possible due to linkages and partnerships between firms across countries. Telecom Company Tigo currently allows for cross-border transfers between Tanzania and Rwanda.21 In December 2015, MTN Uganda and Safaricom signed a mem-orandum allowing for Safaricom mobile money users to trans-fer money into MTN mobile money accounts in Uganda.22

Competition concerns

While expansion and growth of firms is important for contin-ued trade and development in the region, it can also create conditions for certain anti-competitive conduct. In an open, regional market with a regional competition authority it is per-haps less likely for a firm to establish a dominant position other than through mergers and acquisitions. The expectation is that rivals from across the region can more easily compete across borders and undermine the concentration of marketpower at the regional level. However, previous competition cas-es on cartels suggest that cartel conduct is more likely. Many key sectors may be characterised by tight oligopolies in small economies with high entry barriers.23 These characteristics make it likely that incumbent firms will seek to protect their posi-tions through jointly undermining entry, and coordinating pricing and output and allocating markets. In the Southern African Cus-toms Union (SACU) area, a cartel operated in the cement in-dustry between the major multinational firms.

The cement industry in East Africa raises concerns in this re-gard, particularly given that a number of the same firms that were involved in the cartel in SACU are present across coun-tries in East Africa. It has been alleged that the East African Cement Producers Association (EACPA) is used to facilitate collusion between the main producers including firms linked with multinationals Lafarge, Holcim and Heidelberg.24 In SACU, the South African Cement Producers’ Association (SACPA) facilitated information exchange and coordination of output and prices in the entire SACU area, and certain country market were allocated between members.

The lessons from the SACU experience are that certain con-duct may not be detected by individual country authorities and there is a role for monitoring and enforcement by regional au-thorities. This is an important advantage presented by the EACCA which is in a position to enforce across countries. Simi-lar conduct has been identified in South Africa which has had an effect across national borders and in many cases industrial associations have been at the centre of arrangements. Certain arrangements such as those between major producers in the beer industry are candidates for assessment at a regional au-thority level25, and cartels in general should be a focus of a regional body.

Individual mergers that lead to higher concentration in sectors in East Africa may not necessarily be prohibited when consid-ered at a regional level, and may in fact have substantial bene-fits for the region in terms of integration of markets and invest-ment. However, the authority will need to be mindful of ‘creeping’ acquisitions that when considered together increase competition over time. The risks to competition in this case re-sult both from the concentration over time which may allow indi-vidual groups to exercise unilateral market power in the region, and from likelihood that greater concentration may lead firms to agree to coordinate their conduct across borders rather than compete.

The interlinked nature of the economies in the EAC, trade flows, transport linkages and increased economic growth demonstrate the potential for the EAC to develop an integrated regional economy. The potential gains to consumers can be undermined by anti-competitive conduct that is not detected at the cross-country level, which motivates for the introduction of the EACCA.

Notes

- The East African. ‘East African Community to set up authority to push for free, fair trade’ (1 June 2015). The East African.

- East African Community. ‘The East African Community Competi-tion Act, 2006’.

- Bonge, G.M. ‘Towards EAC Competitions Law and Policy’. EABC Briefing Paper, August 2010 Issue 05/10.

- Drexl, J. (2012). Competition policy and regional integration in developing countries. Edward Elgar Publishing.

- See note 4.

- Laperrousaz, A. ‘East- Africa & Antitrust: Enforcement of EAC Competition Act’ (14 January 2016). African Antitrust & Competition Law News & Analysis.

- Mbani, M. ‘In the absence of common competition law…East Afri-can consumers, small producers suffer the most’ (August 2015). Business Times Economic and Financial Weekly.

- The World Bank Data website.

- See note 8.

- Rabisch, S., and Owuor, G. (n.d) ‘Facilitating Well- Functioning Regional Markets in the EAC’.

- East African Community Investment and Private Sector Promotion website.

- East African Community Infrastructure website.

- Burchardt, D. (2009). ‘Why should a country join a customs un-ion?’ GRIN Verlag.

- Nakumatt website.

- Tuskys website.

- Dihel, N. (2011). ‘Beyond the Nakumatt Generation: Distribution services in East Africa’. Policy Note No.26. World Bank.

- See note 10.

- Wagh, S., Lovegrove, A. and Kashangaki, J. ‘Africa Trade Policy Notes: Scaling-up Regional Financial Integration in the EAC’ (July 2011). Policy Note No. 22. The World Bank.

- Kulaboako, F. ‘Airtel buys Warid Telecom‘ (23 April 2013). Daily Monitor.

- Ouma, M. ‘Orange exits Kenya, sells 70% Telkom Kenya stake to Helios’ (10 November 2015). CIO and Malakata, M. ‘With sale to Africell, Orange starts to pull back from East Africa’ (20 November 2014). PCWorld.

- Ng’wanakilala, F. ‘Tanzania's Tigo starts cross-border mobile money transfer service’ (24 February 2014). Reuters.

- Chao-biasto, S. ‘M-Pesa now enters Uganda in Safaricom, MTN pact’ (28 December 2015). Business Daily.

- Vilakazi, T. ‘Editor’s Note’ (August 2014). CCRED Quarterly Competition Review.

- Mbongwe, T., Nyagol, B. O., Amunkete, T., Humavindu, M., Khu-malo, J., Nguruse, G. and Chokwe, E. (2014). ‘Understanding competition at the regional level: An assessment of competitive dynamics in the cement industry across Botswana, Kenya, Namibia, South Africa, Tanzania and Zambia’. African Competition Forum.

- Kaziboni, L. and das Nair, R. ‘The beer industry in Africa: a case of carving out geographic markets?’ (November 2014). CCRED Quarterly Competition Review.